Kelly Criterion for Football Betting: How to Calculate the Optimal Stake

The Kelly Criterion helps bettors determine the optimal stake size based on perceived value and bankroll size. Learn the Kelly formula, see real football betting examples, and understand how to use full, half, or fractional Kelly strategies to maximize long-term growth.

If you've ever wondered how professional bettors decide exactly how much to wager on a match, the answer often comes down to a single mathematical formula: the kelly criterion football betting model. Developed by Bell Labs scientist John L. Kelly Jr. in 1956, the Kelly Criterion isn't a get-rich-quick scheme — it's a rigorous, mathematically proven method for maximising the long-term growth of a betting bankroll while minimising the risk of ruin. On Betiball, we help analytical bettors move beyond guesswork and into a framework grounded in probability and data. This guide breaks down the Kelly formula, shows you how to apply it to football markets, and explains why it remains one of the most powerful tools in a serious bettor's arsenal.

What Is the Kelly Criterion and Where Did It Come From?

The Kelly Criterion was originally designed to solve a problem in information theory — specifically, how to maximise the long-run growth rate of capital when the outcome of each bet is uncertain but the underlying probabilities are known. Kelly published his findings in the Bell System Technical Journal under the title "A New Interpretation of Information Rate," and the formula was quickly adopted by gamblers and investors alike.

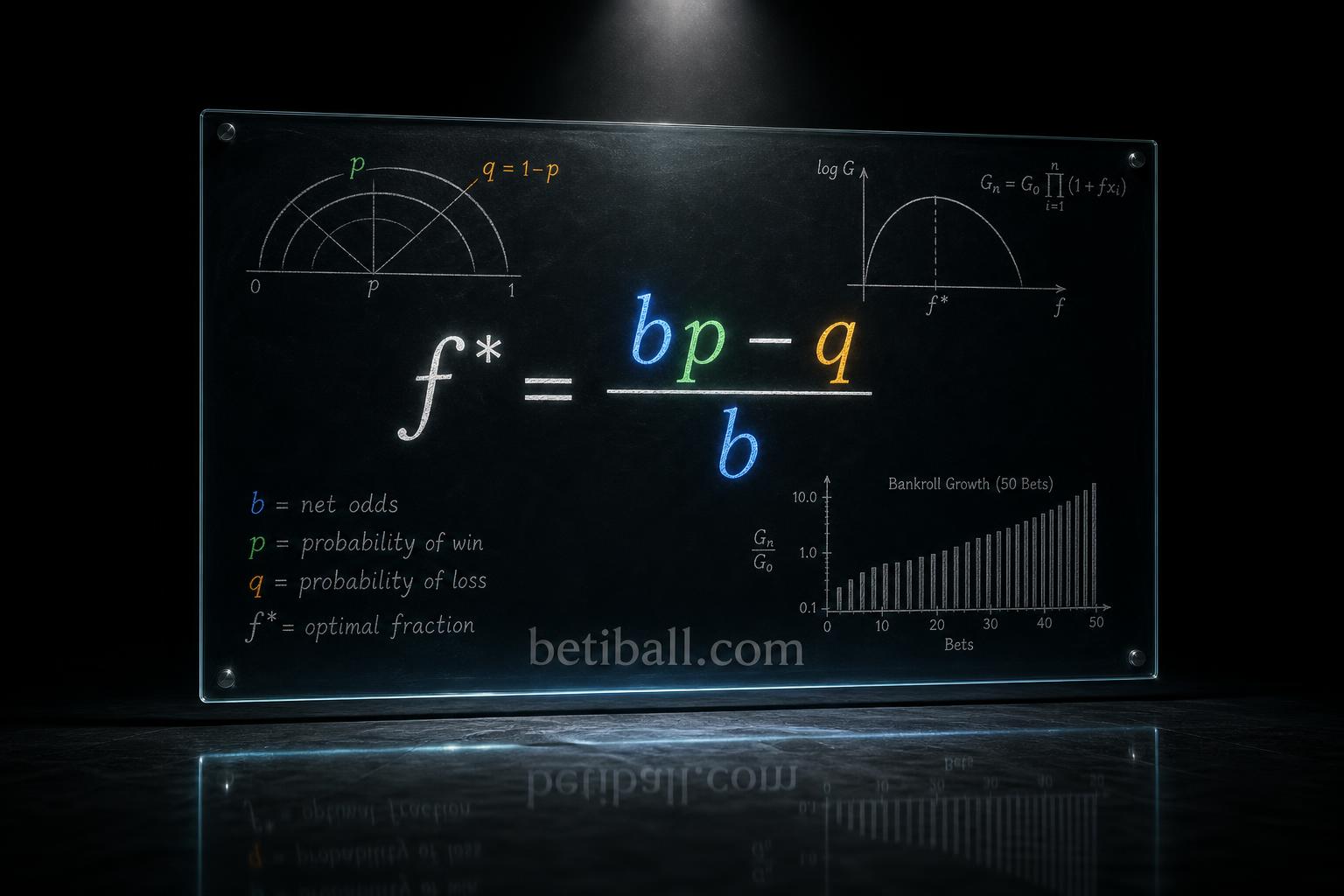

At its core, the Kelly formula answers one precise question: what fraction of your bankroll should you stake on a bet in order to maximise the expected logarithm of wealth over time? The answer is elegant:

f* = (bp – q) / b

Where:

f* = fraction of bankroll to stake

b = net decimal odds minus 1 (i.e., profit per unit staked)

p = your estimated probability of the bet winning

q = probability of losing (1 – p)

In practice, many bettors use the equivalent form written directly for decimal odds:

f* = (p × odds – 1) / (odds – 1)

The formula yields a percentage. If your bankroll is £1,000 and Kelly returns 0.05, you stake £50 on that bet. If Kelly returns a negative number, the model is telling you the bet has no mathematical edge — do not bet.

What makes Kelly especially powerful is its dynamic, self-adjusting nature. As your bankroll grows, stakes grow proportionally. After a losing run, stakes automatically shrink, protecting the bankroll from catastrophic drawdowns. This built-in bankroll management is why the strategy attracts serious, data-driven football bettors.

How to Apply the Kelly Formula to Football Betting Markets

Football presents a unique challenge for Kelly: unlike a coin flip with two discrete outcomes, a typical match has three possible results (Home Win, Draw, Away Win), and markets extend across dozens of bet types — Asian Handicaps, Over/Under totals, both teams to score, and more. Applying the kelly formula betting framework to football requires two preliminary steps before the formula is even used.

Step 1 — Estimate True Probability

The Kelly formula lives or dies on your probability estimate (p). This is not the bookmaker's implied probability — that already contains the overround (margin). You must derive your own model-based probability. Common approaches include:

- Poisson distribution models: Use historical goals-scored and goals-conceded averages to derive expected goals (xG) for each team, then run a Poisson simulation to generate win/draw/loss probabilities.

- Elo rating systems: Assign each team a dynamic rating updated after every result. Convert the rating difference into a win probability using a logistic function.

- Machine learning models: Incorporate broader feature sets — form, squad depth, travel distance, referee data, weather — to generate calibrated probability outputs.

Step 2 — Identify Value

Once you have your probability estimate (p), compare it to the bookmaker's implied probability (1 / decimal odds). If your p is higher, you have a positive expected value (+EV) bet. Only then does Kelly produce a positive f* worth acting on.

Worked Example: Premier League Match

| Variable | Value | Notes |

|---|---|---|

| Bookmaker odds (Home Win) | 2.20 | Decimal odds |

| Implied probability | 45.5% | 1 / 2.20 |

| Your model probability (p) | 52% | Poisson-based estimate |

| b (net odds) | 1.20 | 2.20 – 1 |

| q (loss probability) | 48% | 1 – 0.52 |

| Kelly fraction (f*) | 6.67% | (1.20 × 0.52 – 0.48) / 1.20 |

| Recommended stake (£1,000 bankroll) | £66.70 | f* × bankroll |

At a 6.67% Kelly fraction, the model is flagging genuine edge. A bettor with a £1,000 bankroll would stake £66.70 — neither recklessly large nor negligibly small. If the model had returned p = 45%, Kelly would produce a negative fraction, signalling the bet should be skipped entirely.

Fractional Kelly: Managing Risk in Volatile Football Markets

Even mathematically rigorous bettors rarely use full Kelly stakes. The reason is model uncertainty. The Kelly formula assumes your probability estimate is perfectly accurate — but in football, no model is perfect. If your p is even slightly overestimated, full Kelly can result in stake sizes that create large drawdown swings, even if the edge is real.

The widely adopted solution is Fractional Kelly: applying a fixed percentage of the Kelly recommendation rather than the full fraction. Common choices are:

| Fraction Used | Kelly Stake (from example above) | Recommended Stake (£1,000 bankroll) | Risk Profile |

|---|---|---|---|

| Full Kelly (100%) | 6.67% | £66.70 | Maximum growth, high variance |

| Half Kelly (50%) | 3.34% | £33.40 | Moderate growth, lower drawdowns |

| Quarter Kelly (25%) | 1.67% | £16.70 | Conservative, very smooth bankroll curve |

Research by financial mathematicians including Edward Thorp — who famously applied Kelly to blackjack and financial markets — consistently shows that Half Kelly retains approximately 75% of the long-run growth rate of Full Kelly while dramatically reducing variance and the psychological strain of large swings. For football bettors whose probability models carry meaningful estimation error, Half Kelly is typically the most pragmatic starting point.

Quarter Kelly is appropriate for bettors who are newer to model-based approaches, or where the market being bet on has historically shown high uncertainty in model calibration (e.g., exact score markets, first goalscorer).

Using a Kelly Criterion Calculator: Practical Tools and Their Limits

A kelly criterion calculator automates the formula, requiring only three inputs: your estimated probability, the decimal odds offered, and your current bankroll size. Several free tools exist online, and many serious bettors build their own version in a simple spreadsheet.

Building your own Excel or Google Sheets calculator is straightforward:

- Column A: Your estimated win probability (p)

- Column B: Bookmaker decimal odds

- Column C: Net odds b = B2 – 1

- Column D: Kelly fraction = (C2 × A2 – (1 – A2)) / C2

- Column E: Recommended stake = MAX(D2, 0) × Bankroll

The MAX function in Column E is critical — it prevents the calculator from recommending a negative stake, outputting £0 for any no-edge bet.

The limits of any kelly criterion calculator are the same limits as the formula itself: the output quality is entirely determined by your probability inputs. Bettors who feed overconfident probability estimates into the calculator will systematically over-stake, accelerating bankroll erosion rather than growth. This is sometimes called "Kelly's curse" — the formula is only as good as the model behind it.

Best practice is to back-test your probability model over a historical dataset of at least 300–500 matches before applying Kelly stakes with real money. Track not just win rate but calibration — does your model's 60% confidence level actually win approximately 60% of the time? Tools like Brier scores and reliability diagrams help validate this.

Optimal Stake Betting: Kelly Versus Alternative Strategies

It's worth situating Kelly within the landscape of optimal stake betting strategies to understand where it truly excels — and where flat-staking or other methods may be preferable.

| Strategy | Stake Method | Pros | Cons |

|---|---|---|---|

| Flat Staking | Fixed £ per bet | Simple, low variance | Does not scale with bankroll; ignores edge size |

| Fixed Percentage | Fixed % per bet (e.g., 2%) | Simple, auto-scales | Ignores edge magnitude; all bets treated equally |

| Kelly Criterion | Variable % based on edge and odds | Mathematically optimal long-run growth; accounts for edge size and odds | Requires accurate probability estimates; high variance at full Kelly |

| Martingale | Doubles after each loss | Short-run recovery illusion | Catastrophic ruin risk; mathematically indefensible long-term |

| Value-Proportional | Stakes proportional to edge size | Intuitive edge scaling | Does not account for odds level; less precise than Kelly |

Kelly's theoretical superiority is well-documented: given accurate probability estimates, no strategy produces higher long-run bankroll growth. However, for bettors who

Your feedback helps us deliver better football betting insights.